Original briefings. Zero spin.

Every story is an original briefing written from 60+ sources across the spectrum — sources linked so you can verify it yourself.

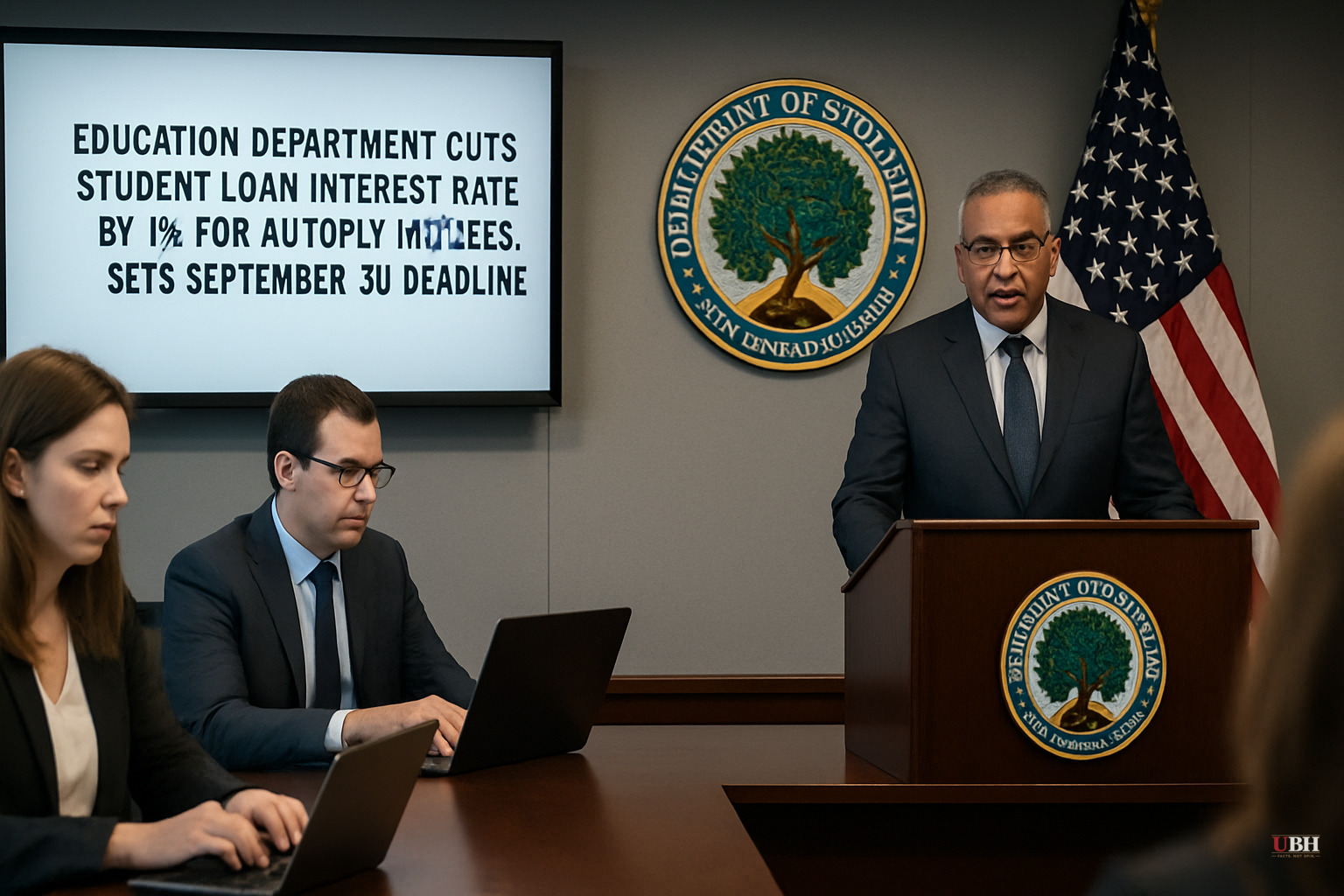

Education Department Cuts Student Loan Interest Rate by 1% for Autopay Enrollees, Sets September 30 Deadline

What the Department Actually Did

The Department of Education announced last week that federal student loan borrowers who enroll in autopay — automatic deductions from a checking or savings account — by September 30, 2026 will receive a 1% interest rate reduction. That's four times the old 0.25% discount that previously existed for the same enrollment.

The practical effect: lower monthly payments and less total interest paid over the life of the loan. The department's stated goal is straightforward. Get more borrowers actually paying their loans.

The Repayment Gap Is Real

According to the Department of Education, only 40% of federal student loan borrowers are currently enrolled in autopay. Before the COVID-19 pandemic, that figure was above 80%. That collapse in participation has degraded what the department calls the "overall health of the federal student loan portfolio."

With approximately $1.7 trillion in outstanding federal student loan debt, even marginal improvements in repayment rates carry significant fiscal weight. A larger percentage of borrowers in active repayment means fewer defaults, less pressure on taxpayers, and a more stable loan portfolio.

What This Is Not

This is NOT broad debt cancellation. It doesn't touch principal balances. It doesn't forgive anything. It is a targeted incentive: cut your interest bill by enrolling in automatic payments, with a hard deadline attached.

This differs from the approach taken by the Biden administration, which pursued large-scale forgiveness programs that were repeatedly blocked. As the Daily Signal analysis notes, America's student loan crisis cannot be solved by "repeatedly transferring debt from borrowers to taxpayers, as the previous administration attempted multiple times."

The Strongest Case for a Bigger Fix

Critics on the left would fairly argue that a 1% autopay discount does nothing for the millions of borrowers who can't afford any payment at all, regardless of interest rate. For someone with significant debt and a modest salary, shaving a percentage point off the interest rate doesn't make the payment manageable. They'd argue the real problem is that tuition has outpaced wages for decades, and that nibbling at interest rates while leaving the principal and the underlying cost spiral untouched amounts to policy theater.

The 40% autopay participation rate isn't just apathy. Some portion of the borrowers who dropped out of autopay did so because they couldn't sustain payments after pandemic-era forbearance ended.

The counter is that the Biden administration's repeated attempts at mass forgiveness — blocked by courts each time — didn't solve the structural problem either. They transferred existing debt to taxpayers without reforming the system that generates new debt every year. Neither blanket forgiveness nor minor incentive tweaks address tuition inflation or whether specific degree programs produce graduates who can repay what they borrowed.

The College Accountability Piece

The Daily Signal's analysis, written by Ella Jackson and Madison Marino Doan, frames this correctly. The debt crisis has two sides. Borrowers who voluntarily took out loans have an obligation to repay them. But institutions that expanded enrollment into programs with weak job outcomes — while tuition climbed — bear responsibility too.

For decades, colleges have had little financial skin in the game when graduates default. The borrower defaults, the federal government eats the loss, and the university keeps its accreditation and its federal funding. That structure creates obvious perverse incentives.

The Foundation for Research on Equal Opportunity, in a recent report reviewing the return on investment for 53,000 different degree and certificate programs, found that "around a third of federal Pell Grant and student loan funding pays for programs that do not provide students with a return on investment," and that "nearly half of master's degree programs leave students financially worse off."

The McMahon-led Education Department has not yet announced specific institutional accountability measures alongside this autopay incentive. Whether colleges will face consequences tied to graduate repayment rates remains an open policy question under the current administration.

What Happens After September 30

The department has labeled this a temporary measure, which raises a question the announcement doesn't answer. Does the 1% reduction expire after a fixed period, or is it locked in for the life of the loan once a borrower enrolls?

The terms of duration matter enormously to a borrower deciding whether to reorganize their finances around autopay. The Department of Education has not publicly clarified that detail, according to available sources.

Sources used for this briefing

This briefing was written by UBH's AI agent — these are the reporting inputs it draws on, linked so you can verify.