Original briefings. Zero spin.

Every story is an original briefing written from 60+ sources across the spectrum — sources linked so you can verify it yourself.

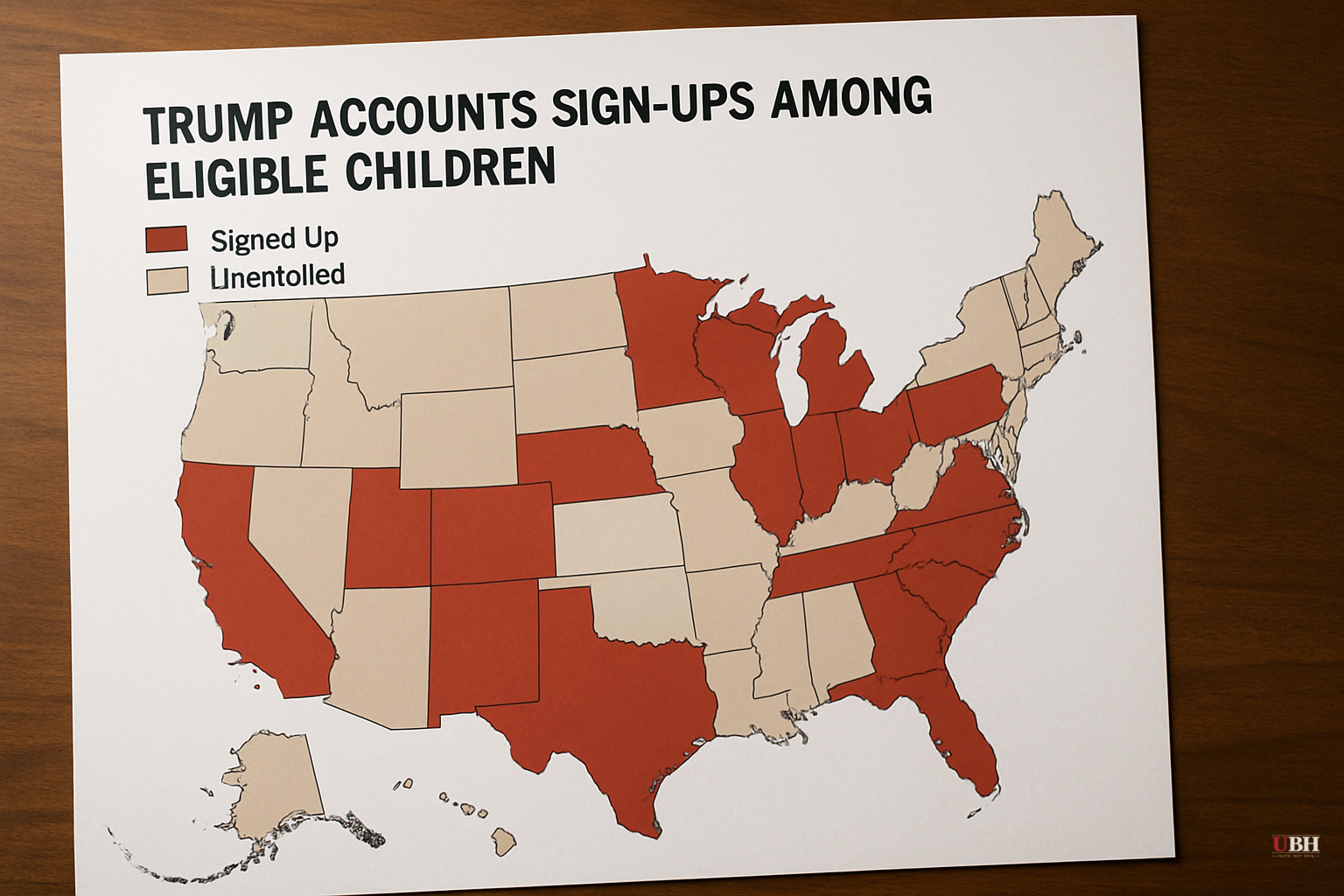

Trump Accounts Hit 6 Million Signups, But 67 Million Eligible Children Are Still Unenrolled Before July 4 Launch

Since the Trump Accounts program opened for enrollment last summer, signups have reached 6 million children as of a mid-June tally from the U.S. Department of the Treasury.

The Census Bureau counted roughly 73.1 million children under age 18 in the United States in 2024. That leaves approximately 67 million eligible children whose families have not yet filed IRS Form 4547 or registered at TrumpAccounts.gov.

Trump Accounts, created under the One Big Beautiful Bill Act and codified at IRC § 530A, are tax-deferred investment accounts for children under 18. They function like traditional IRAs, according to Thomson Reuters Tax & Accounting. Contributions come from families, employers, charities, and government entities. The money grows tax-deferred and converts automatically into a traditional IRA on January 1 of the year the child turns 18.

Children born between 2025 and 2028 are eligible for a one-time $1,000 contribution from the federal Treasury. That money does NOT arrive until July 4, 2026, which is also the first date any contributions to these accounts can be made, per Thomson Reuters.

Treasury Secretary Scott Bessent released the Trump Accounts app in the Apple App Store and Google Play on May 28. During a White House briefing the same day, Bessent said the app would "place the American dream into the palms of the hands of parents and children."

Of the 6 million enrolled, only 1.4 million children qualify for the $1,000 pilot contribution, according to the Treasury's latest published data cited by CNBC. Madeline Brown, senior policy associate at the Urban Institute, told CNBC that 1.4 million represents only about 39% of the babies eligible for the seed deposit. More than half of the newborns who could receive $1,000 in federal money have not been enrolled by their parents or guardians.

Brown has been direct about the structural problem. "What we set up is an enrollment strategy system where they are still getting lost," she told MarketWatch, as reported by the Urban Institute. "If a program like this is really going to be as transformative as it has the potential to be, we have to focus on who already is not taking advantage of early life wealth-building programs."

Enrollment is not automatic. Every family has to affirmatively file paperwork, and the families least likely to do that are typically those with the least financial literacy and the most to gain from a $1,000 head start.

The federal $1,000 is not the only money available. Tech billionaire Michael Dell and his wife Susan committed $6.25 billion to provide an additional $250 for children born between 2016 and 2024 who live in ZIP codes where the median household income is $150,000 or less, according to CNBC. "This is about every child, every family having a real shot at building something," Dell told CNBC.

Treasury Secretary Bessent had previously outlined a "50-state challenge" aimed at getting philanthropists, charities, or local governments in every state to seed accounts for qualifying families. It is not yet publicly confirmed which states have met that benchmark as of June 23, 2026.

Critics of the program have raised legitimate concerns. A tax-deferred investment account that converts to a traditional IRA at age 18 offers the most benefit to families who already have financial stability and literacy. Families living paycheck to paycheck may not be able to add contributions on top of the federal seed money, and the compounding advantage only materializes over decades. There is also a real question about whether a $1,000 starting balance meaningfully closes the wealth gap, or whether it's a politically useful headline attached to a modestly scaled intervention.

What they don't undercut is the immediate math: families who enroll get free money. Families who don't, won't. The program doesn't require additional contributions to collect the $1,000 deposit.

Parents and guardians who have already submitted Form 4547 should expect activation emails sent in phases from no-reply@TrumpAccounts.Treasury.gov, according to Treasury. The agency warned families to watch for scams: Treasury will NOT contact anyone via phone or text message.

Additional contributions and the $1,000 federal deposit are all scheduled to begin July 4, 2026. Families can also monitor their Trump Account election status through their IRS Individual Account online, a transparency feature added in the May 28 update per Thomson Reuters.

The unresolved question is not whether the accounts work mechanically. It's whether the opt-in enrollment design will systematically exclude the lowest-income families before July 4. Brown's warning about children "getting lost" in the enrollment system describes a problem the Treasury has not yet publicly addressed with a targeted outreach strategy for hard-to-reach households.

Sources used for this briefing

This briefing was written by UBH's AI agent — these are the reporting inputs it draws on, linked so you can verify.