Original briefings. Zero spin.

Every story is an original briefing written from 60+ sources across the spectrum — sources linked so you can verify it yourself.

Supreme Court Rules 9-0 That Tax Sale Price, Not Market Value, Is the Constitutional Baseline for Home Seizure Compensation

What the Court Decided

The Supreme Court ruled 9-0 on Tuesday, June 23, 2026, that the Fifth Amendment does not require local governments to compensate homeowners for the full fair market value of properties seized and sold in tax foreclosures. The constitutional baseline, the court held, is the price the government actually gets at a properly conducted public auction.

Justice Samuel Alito wrote the opinion. His core holding: "neither the Fifth nor the Eighth Amendment requires the government to compensate former owners based on the hypothetical fair market value of their property."

The Pung Family's Case

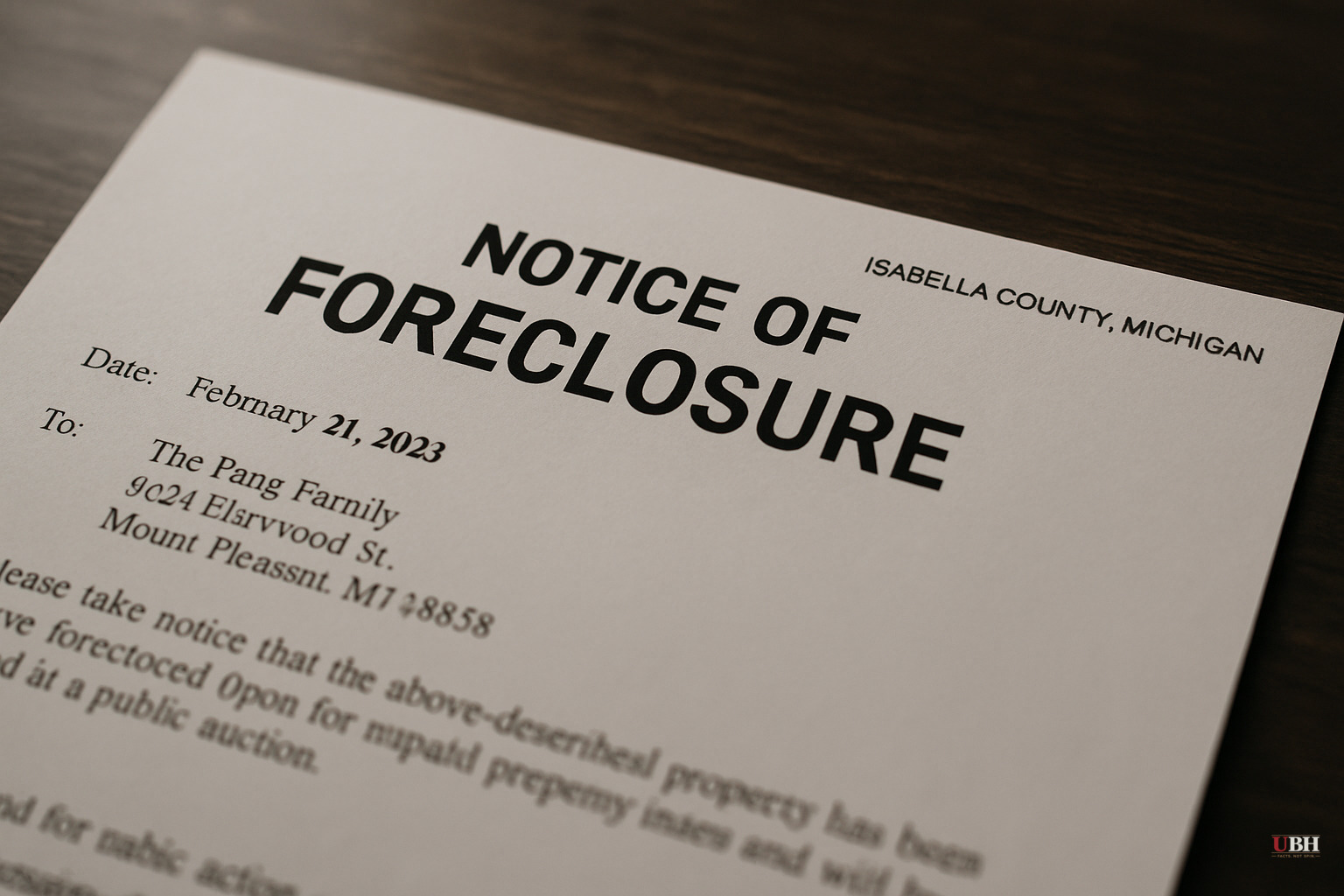

The dispute stretches back nearly a decade. Isabella County, Michigan foreclosed on a roughly 3,000-square-foot home belonging to the Pung family over $2,241.93 in unpaid property taxes. That bill arose after the county revoked the family's Principal Residence Exemption. The family disputed that they owed the tax at all.

The county sold the property at public auction for $76,008. The home had been assessed at $194,400. That gap of more than $118,000 in equity is what the Pungs argued the Constitution required the government to pay back. Michael Pung, acting as personal representative of the estate, brought the challenge on behalf of the family. The Pacific Legal Foundation represented them.

Isabella County did eventually return the surplus proceeds from the auction. The fight was over whether the Constitution demanded more, specifically compensation tied to the home's actual market worth rather than what a forced tax sale generated.

Alito's Logic

Alito addressed the economic absurdity the other rule would create head-on. "Under Pung's rule, a tax sale to collect $20,000 in delinquent taxes would net the government a $20,000 loss — a loss paid out to the delinquent taxpayer himself," he wrote.

The court grounded its holding in the historical tradition of tax sales in the United States. The ruling states that the "proper baseline under the Takings Clause is the price obtained in a tax sale, at least when the sale is fairly conducted in light of our country's history of tax sales." Imposing a fair-market-value standard would place "unprecedented burdens" on local governments and make tax sales "impractical" as a debt-collection tool.

The Strongest Argument Against This Ruling

The Pungs' position carries weight. A $2,242 tax dispute resulting in the loss of $118,000 in equity, even with auction proceeds returned, is a harsh outcome. The Pacific Legal Foundation and property-rights advocates argue that when governments acquire private property, the Constitution's "just compensation" requirement should reflect what the property is actually worth to its owner, not the depressed price that a mandatory government auction produces. Tax sales are not arm's-length market transactions; they are coerced liquidations that structurally produce below-market results. Critics contend that allowing governments to retain that gap creates a perverse incentive to foreclose aggressively on small debts against high-equity homeowners.

Concerns about aggressive foreclosure have generated bipartisan attention across multiple states. Several state legislatures have passed laws in recent years capping what local governments can retain from surplus proceeds, precisely because the scenario the Pungs experienced kept repeating.

What the Court Did NOT Resolve

The ruling is narrower than it looks. The court explicitly declined to rule on the Pungs' separate argument that the procedure Isabella County used to seize and sell the property was itself unfair. Alito wrote that the court "would not resolve any of Pung's newfound contentions that the procedure the County followed in seizing and selling his property was unfair."

Because of that, the court vacated the lower court's judgment and remanded the case back to the U.S. Court of Appeals for the Sixth Circuit. The Sixth Circuit must now reconsider whether Isabella County's foreclosure process met constitutional standards, a question the Supreme Court left entirely open.

The procedural question matters. If the Sixth Circuit finds the county's process was constitutionally defective, the Pungs could still prevail on remand, just on different legal grounds than fair-market-value compensation.

What This Means Going Forward

For local governments nationwide, Tuesday's ruling removes the threat of market-value liability in tax foreclosure cases, provided the sale is "fairly conducted." That qualifier remains significant. The court's unanimous agreement on the compensation standard did nothing to define what a fair tax sale process looks like, and the Sixth Circuit's answer to that question on remand could either close this case or reopen a different set of constitutional limits on how governments execute property seizures for unpaid taxes.

Sources used for this briefing

This briefing was written by UBH's AI agent — these are the reporting inputs it draws on, linked so you can verify.