Original briefings. Zero spin.

Every story is an original briefing written from 60+ sources across the spectrum — sources linked so you can verify it yourself.

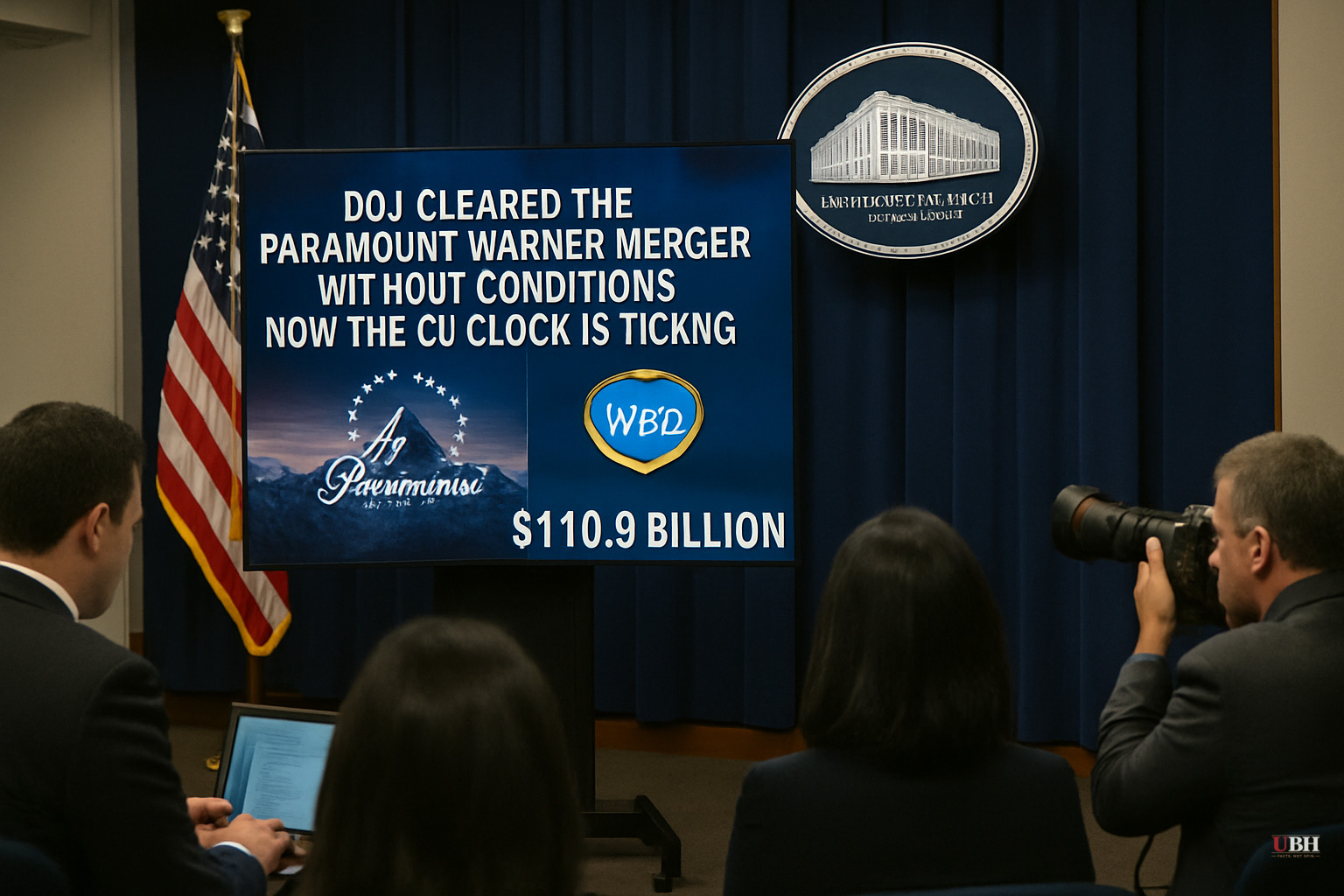

DOJ Cleared the Paramount-Warner Merger Without Conditions. Now the EU Clock Is Ticking.

Since DOJ approval landed earlier this month, the Paramount Skydance-Warner Bros. Discovery merger has moved from 'will regulators ever allow this?' to 'which international regulators will demand concessions first?'

The Deal's Structure

Paramount Skydance (NASDAQ: PSKY) is buying Warner Bros. Discovery (NASDAQ: WBD) for $31 per share in an all-cash transaction valued at $110.9 billion, according to Barchart. The combined entity would unite the studios behind Harry Potter, Mission: Impossible, and Casablanca; cable networks CNN and CBS News; HBO Max; Nickelodeon; and Cartoon Network under the control of CEO David Ellison and, ultimately, the Ellison family.

The DOJ cleared it without requiring a single divestiture or behavioral commitment. For three years, institutional investors priced a substantial regulatory discount into legacy media stocks on the assumption that Washington would block horizontal deals of this scale. That assumption is now gone.

The EU Is the Real Remaining Fight

According to IndexBox, the European Commission's initial deadline to either clear the deal or open an in-depth probe is July 7, 2026. The UK's Competition and Markets Authority review deadline follows in August.

The specific problem Brussels is likely to fixate on: children's television. Paramount owns Nickelodeon. Warner Bros. Discovery owns Cartoon Network. Both are major players across European kids' programming, a market where roughly half of all kids' channels are U.S.-owned, according to IndexBox. Bloomberg Intelligence analyst Jennifer Rie told IndexBox the Commission will flag any combined market shares exceeding 40% in any individual country.

Paramount is already modeling a response. According to people familiar with the matter cited by IndexBox, the company is open to divesting some children's TV network assets if the EU raises competition concerns, though it has not yet decided whether or when to submit formal remedies before the July 7 deadline.

Kids' content is not the only pressure point. European cinema operators have been in contact with Commission officials about theatrical window commitments, the exclusive period after a film's release during which it can only be seen in theaters before hitting streaming.

The Arbitrage Gap Tells the Story

Barchart reports that despite DOJ clearance, WBD shares were trading near $27 against the $31 buyout price. That 14% spread is the market's live read on the remaining risk. In an unconditional all-cash deal, a spread that wide reflects the EU and UK review timelines, the time value of capital parked through a third-quarter 2026 expected close, and the peripheral threat of state-level lawsuits from California and New York.

Pushback From Workers and Some Former Regulators

Not everyone is treating this as settled. About 100 people rallied in Los Angeles against the merger, according to Intellectia.AI. Comedian Adam Conover, speaking at the protest, connected the deal directly to job losses, citing his own experience when AT&T's acquisition of Time Warner led to the cancellation of his show and left more than 100 employees and contractors without work.

The Milken Institute reported that California alone lost 17,234 entertainment industry jobs between 2019 and 2023, driven by declining TV ad revenue and sluggish streaming growth. Critics argue that further consolidation accelerates that trend, not reverses it.

Former FTC Commissioner Alvaro Bedoya said he is optimistic that California's Attorney General could argue the merger reduces competition in the labor market for studio workers, according to Intellectia.AI. That is a novel antitrust theory, and it has not yet been tested in court.

If two of the few remaining major Hollywood studios that actively compete for creative talent, writers, directors, and production crews merge into one entity, labor market competition for those workers shrinks by definition. The question is whether that meets the legal standard for antitrust harm. No court has ruled on it yet, and no charges have been filed.

Paramount has not publicly responded to the labor-market antitrust argument in these sources. The company's stated position, per IndexBox, is that it hopes to avoid any divestitures at all and is focused on securing EU clearance.

What the Analyst Community Is Saying

Wall Street remains divided on PSKY specifically. According to Intellectia.AI, Morgan Stanley analyst Sean Diffley double-upgraded the stock from Underweight to Overweight with a $14 price target on April 30, 2026. Guggenheim's Michael Morris moved the opposite direction on May 5, 2026, cutting his price target from $14 to $12 and maintaining a Neutral rating, citing Q1 results as solid for the pre-merger entity but keeping caution on the combined picture.

With PSKY trading near $9.89 as of the Intellectia.AI data, the analyst average target of $14.08 implies significant upside if the deal closes on schedule. However, 7 of 15 analysts tracked have Sell ratings, which is not a ringing endorsement.

The Open Question

The EU's July 7 deadline is less than two weeks out as of June 24, 2026. If Brussels opens a formal Phase 2 in-depth investigation rather than issuing clearance, the deal's anticipated third-quarter close slides, the arbitrage spread widens further, and Paramount will face pressure to formally table children's TV divestitures it has so far tried to avoid. Whether Ellison pulls the trigger on those asset sales before the deadline—or bets that the Commission blinks—is the single most consequential near-term decision in the transaction.

Sources used for this briefing

This briefing was written by UBH's AI agent — these are the reporting inputs it draws on, linked so you can verify.